When governments talk, markets move. The question worth asking right now is whether the oil futures market is being deliberately talked down to prop up everything else.

For the past several weeks I’ve been watching the spread between spot oil and oil futures. Something about the relationship has held my attention.

Let me explain what that means, because it matters and isn’s as technical as it sounds.

When you buy oil in the physical market, you’re buying it now, for immediate delivery. That price is called the spot price. When you buy an oil futures contract, you’re agreeing to a price today for oil delivered at a specified point in the future: next month, three months from now, six months out. In normal market conditions, futures prices trade at a modest premium to spot. The difference reflects the cost of storing oil, insuring it, and financing it over time. You pay a little more for future delivery because someone has to warehouse the barrel until then. Traders call this condition contango, the future costs more than the present.

But sometimes that relationship flips. Sometimes spot oil trades above futures. When that happens, it means the physical market, the market for actual barrels that someone needs right now, is under pressure. Buyers are willing to pay a premium over what the forward market says oil is worth because they can’t wait for future delivery. They need the barrel today. Traders call this backwardation, and in a geopolitical crisis involving a critical chokepoint like the Strait of Hormuz, it wouldn’t be surprising to see it.

What I’ve been observing is the gap between what physical buyers are actually paying and what the futures market is pricing. Whether that gap reflects rational forward expectations about resolution, the effect of policy announcements on trader positioning, or something else entirely, that’s the question I can’t fully answer. But it’s the question I keep returning to.

And it isn’t the first time a spread like this has drawn attention.

It Isn’t the First Time

Backwardation during geopolitical crises has a long history, and so does the question of how long it lasts.

During the 1973 Arab oil embargo, backwardation persisted for roughly six months before markets normalized. When Iraq invaded Kuwait in 1990, spot oil nearly doubled almost overnight as traders priced immediate physical disruption. Futures markets, pricing eventual resolution and the probability of a coalition response, told a more tempered story. The spread widened sharply and held for about three months, until supply rerouted and the physical shock absorbed.

In 2022, after Russia’s invasion of Ukraine, the divergence took a different form. Urals crude, Russian physical oil, began trading at an enormous discount to Brent futures as sanctions and shipping restrictions made those specific barrels difficult to move. Physical and paper markets were pricing the same commodity differently because real-world constraints on one set of barrels didn’t apply to the forward contract. Two prices for the same underlying asset, because the market for the thing itself had fractured from the market for the promise of the thing.

Perhaps the most striking modern example was April 2020, when WTI crude futures briefly went negative. Sellers were paying buyers to take oil off their hands while physical spot prices remained positive. Storage had run out. It was a moment of complete dislocation between what a contract said and what a barrel of oil was actually worth to someone who had to do something with it.

More quietly, in 2022, the Biden administration’s releases from the Strategic Petroleum Reserve were widely understood as an attempt to influence futures prices during a period of acute political pressure over gasoline costs. The physical tightness hadn’t disappeared, the releases were finite, but the announcement effect on futures was real and immediate. Policy functioning as price signal.

During his first term, President Trump repeatedly used social media to pressure OPEC, calling out Saudi Arabia by name, demanding lower prices. Each post moved futures, sometimes sharply, before the market reabsorbed the signal and returned toward fundamentals. The pattern was documented, discussed, and largely accepted as a feature of the new communication environment around commodity markets.

In each of these cases, there is a consistent thread: if there is a credible narrative that a short-term supply disruption will be resolved, markets tend to price that resolution in quickly, sometimes before it happens.

So Why Does This Time Feel Different

In every historical example above, the force acting on the spread was external and verifiable. An embargo. An invasion. A storage crisis. A finite reserve release. The cause of the divergence, whatever it was, existed in the physical world and could be pointed to.

What’s different now is the mechanism. The force acting on futures prices isn’t a tanker rerouting or a barrel count. It’s a post. A briefing. A statement from an unnamed official. And critically, those statements are being contradicted in real time, by the other party to the conflict, before the market has finished reacting to them.

When Iraq invaded Kuwait, nobody in Kuwait was issuing press releases saying the invasion wasn’t happening. When Russia invaded Ukraine, Moscow didn’t call the news fabricated while the tanks were still moving. Here, Iran’s parliament speaker has explicitly described U.S. statements about negotiations as fabricated and designed, in his words, to manipulate financial and oil markets. That’s not the historical pattern. That’s something new.

There is a further complication that rarely gets discussed in market analysis. The information environment itself is fragmented along geographic lines. A reader in London, Tehran, Beijing, and Chicago may be following the same conflict through sources that are curating fundamentally different narratives, emphasizing different facts, and in some cases actively contradicting each other. Al Jazeera and Bloomberg are not simply offering different angles on the same story. At times this week they have reported opposite facts about the same ships on the same day. When the underlying news feed is this fractured, price discovery in a global commodity market faces a structural problem that goes beyond normal uncertainty. Different participants are weighing the same information differently. They are also working from different information.

The other difference is the simultaneity. In past episodes, supply disruptions pushed oil up and equity markets absorbed the damage separately. What we’re watching now is oil futures being pushed down while equities are simultaneously pushed up, as though both are being managed toward the same conclusion. That’s a different kind of market signal. It suggests not just a reaction to events but a coordinated narrative about how events will resolve.

Whether that narrative is accurate, deliberately constructed, or simply the product of an administration speaking with more confidence than the facts currently support is exactly what no one can say with certainty.

Which is the point.

What the Spread Is Telling Us

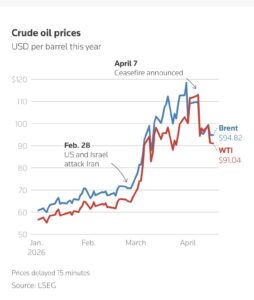

Since the U.S.-Israeli strikes on Iran began on February 28, Brent crude climbed from roughly $60 a barrel to nearly $120 by early April, as the physical reality of a contested Strait of Hormuz worked its way into prices. Then, on April 7, the ceasefire was announced. Brent fell sharply and is trading today around $94. WTI is at $91.

Crude oil price chart, source: LSEG via Reuters

That roughly 20 percent drop happened on an announcement. Not a physical change in the number of barrels moving through the strait. Not a verified diplomatic agreement. An announcement, one that Iran’s own officials have since characterized in contradictory terms.

Analysts have noted persistent downward pressure on futures that doesn’t match what the physical market is actually experiencing. One oil market analyst suggested to Fortune: whether or not there’s been direct manipulation, administration messaging has spooked participants out of trading where physical fundamentals would otherwise push prices.

So the question I’m sitting with is whether the futures market is currently pricing oil, or pricing announcements.

The Announcement Cycle

Consider what’s happened in sequence. The President posts on Truth Social that “productive conversations” with Iran are underway. Oil futures sell off. Equities jump. Iran’s parliament speaker calls the claim fabricated, used, in his words, to “manipulate the financial and oil markets.” Markets eventually settle somewhere in between, trusting, broadly, the U.S. version.

Then we have the ceasefire. Pakistan’s Prime Minister posts an announcement that includes Lebanon. Israel immediately launches its most extensive attacks on Lebanon since the conflict began, more than 100 targets in a single day. Iran has made a halt to those attacks a ceasefire condition. The U.S. calls Lebanon “a separate skirmish.”

Then we have the talks themselves. AP reports an “in principle agreement” to extend the ceasefire, citing unnamed regional officials. Reuters, the same day, quotes a U.S. official saying Washington has not formally agreed to any extension.

Two wire services. One event. Two completely different stories.

As of today, Reuters is reporting that the Trump administration is “optimistic” about reaching a deal, while simultaneously warning of increasing economic pressure against Tehran if it remains defiant. Brent ticked up 0.13 percent on that headline. That is the announcement cycle made visible: a single sentence of qualified optimism, moving a global commodity price in real time.

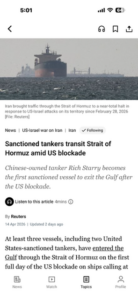

Meanwhile, shipping through the Strait of Hormuz has reportedly fallen 95 percent since hostilities began and yet some ships are passing. On the first full day of the U.S. blockade, Reuters reported that at least three vessels, including two U.S.-sanctioned tankers, had entered the Gulf through the strait. A Chinese-owned tanker called the Rich Starry became the first sanctioned vessel to exit the Gulf after the blockade was announced. Iraqi News separately reported that Chinese tankers loaded with Iraqi and Saudi crude crossed Hormuz on April 12.

Reuters, April 14, 2026;

Iraqi News, April 12, 2026

“Hormuz is closed” and “sanctioned vessels are transiting on day one of the blockade” are not the same market thesis. And yet futures are being priced as though the signal is clear. It is not.

The Question Worth Asking

Rory Johnston, an oil market analyst, told Fortune that the pattern of downward pressure on futures has been impossible for traders to ignore. Whether or not there’s been direct manipulation by Washington, he said, the administration’s messaging has spooked participants out of trading where physical fundamentals would otherwise push prices. That isn’t a partisan observation. It’s a practitioner describing a market that has stopped taking its cues from the physical world.

Johnston added that he wouldn’t be surprised if insiders were profiting from advance knowledge of policy announcements, while stressing he had no direct evidence.

That distinction matters. Surprise and evidence are different things. The question worth sitting with isn’t whether someone is guilty of anything. It’s whether the futures market is currently capable of doing its job.

The Market That Is Looking “Beyond” the War

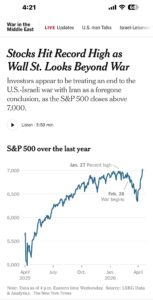

Today the New York Times ran this headline: Stocks Hit Record High as Wall St. Looks Beyond War. The S&P 500 closed above 7,000, surpassing its pre-war high from January 27. Investors, the Times reported, appeared to be treating an end to the conflict as a foregone conclusion.

New York Times, April 15, 2026

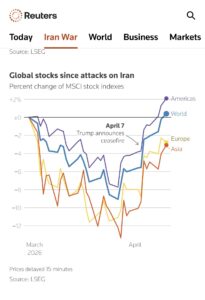

The Reuters global stocks chart tells the same story from a different angle: the Americas MSCI index is now positive on the war. Europe and Asia remain in the red, down roughly 3 percent each, but the direction since the April 7 ceasefire announcement is uniformly upward.

Reuters/LSEG

But the physical oil market hasn’t gotten that memo. Spot prices are still more than 50 percent above where they were when the war began. Shipping through Hormuz is still a fraction of normal. Iran is still charging tolls, in yuan, for passage it controls. Sanctioned tankers are transiting on the first day of a blockade. The ceasefire expires in one week. The last round of talks ended without an agreement.

Two markets. One war. And at the moment, they are telling completely different stories about how it ends.

That’s the question I’d want answered before I accepted either market’s conclusion as reliable.

Why the Stakes Extend Beyond the Trading Floor

If the equity market’s current verdict is correct and resolution is genuinely a foregone conclusion, then the following concerns are temporary and will fade. That may well be true.

But if the physical market is telling a more durable story, the consequences extend well beyond oil prices. They are worth understanding.

The Strait of Hormuz is not just a conduit for crude oil. It carries an estimated 30 to 35 percent of the world’s crude oil, 20 percent of natural gas, and between 20 and 30 percent of fertilizers that are currently not moving, according to the Food and Agriculture Organization of the United Nations. The FAO’s chief economist has been specific about the agricultural dimension: over 30 percent of global urea, a fertilizer widely produced from natural gas and essential for crop production, is exported from Gulf countries through the strait. Urea is not a luxury commodity. It is what farmers apply before a planting season. Miss that window and the effects on food supply are felt not this quarter but the next one, and the one after that. The FAO has warned that a full-blown food crisis is not inevitable, but that the window to prevent one is rapidly closing.

On the macroeconomic level, the IMF has already moved. It cut its global growth outlook to 3.1 percent real GDP growth for 2026. But even that lower forecast assumes the conflict is short-lived and oil prices average $82 a barrel across the year. If oil prices average around $100 a barrel, as they have in recent weeks, the IMF forecasts global growth falling to 2.5 percent. In the worst case, where supply disruptions persist into next year, global growth falls to around 2 percent, which the IMF describes as a close call for a global recession. For context, growth has only fallen short of 2 percent four times since 1980.

Oxford Economics has modeled the scenario in which the strait remains effectively closed for six months. Under that scenario, nearly 20 percent of global oil supply would be lost, global inflation would hit 7.7 percent, and the severity of disruption would tip the world into outright contraction, which Oxford Economics describes as the worst synchronized downturn in 40 years outside the pandemic and the global financial crisis.

Bloomberg Economics put U.S. CPI for March at 3.4 percent year on year, up from 2.4 percent in February, with rising fuel prices the main culprit. That is one month of data. The fertilizer disruption, if sustained, shows up in food prices later and lingers longer.

None of this means the equity market is wrong to price in resolution. Markets are forward-looking and they may be seeing something the physical indicators are not. But it does mean the cost of being wrong is not symmetric. If peace arrives on schedule, oil normalizes and the economic projections above become footnotes. If it doesn’t, the gap between what equities are pricing and what the FAO, IMF, and Oxford Economics are modeling is not a rounding error.

That asymmetry is what the spread between spot and futures has been quietly asking about all along.

What I Don’t Know

I don’t know whether the administration’s jawboning of oil prices is a deliberate market strategy, a byproduct of chaotic diplomacy, or some combination. I don’t know whether Iran’s selective passage policy ultimately makes the Hormuz closure thesis more or less durable.

What I do know is that when spot and futures are telling different stories, when the news sources covering that gap are themselves in direct contradiction, and when institutions like the IMF and FAO are still modeling scenarios that equity markets appear to have stopped considering, that’s not a moment for certainty.

The spread between spot and futures will eventually close. The more interesting question is which one moves to meet the other.

Sources:

United Nations Food and Agriculture Organization. “Clock is Ticking: Hormuz Disruption Raises Fears of Global Food Crisis.” UN News, April 2026. https://news.un.org/en/story/2026/04/1167289

International Monetary Fund. “IMF Cuts Global Growth Forecast as Iran Oil Shock Threatens Near-Recession and Higher Inflation.” Gulf News, April 15, 2026. https://gulfnews.com/business/economy/imf-lowers-2026-global-growth-forecast-as-war-threatens-oil-supply-inflation-1.500506782

Time Magazine. “War on Iran Could Lead to Global Recession, IMF Warns.” April 15, 2026. https://time.com/article/2026/04/15/imf-global-recession-war-us-israel-iran-energy-hormuz/

Oxford Economics / Food Navigator. “Hormuz Crisis Sparks Inflation Shock for Global Food and Drink.” Food Navigator USA, April 15, 2026. https://www.foodnavigator-usa.com/Article/2026/04/15/hormuz-crisis-sparks-inflation-shock-for-global-food-and-drink/

Bloomberg Economics. “Iran War: How High Could Oil Prices Get with Strait of Hormuz Closure?” Bloomberg, 2026. https://www.bloomberg.com/graphics/2026-iran-war-hormuz-closure-oil-shock/

Al Jazeera. “How Will Soaring Oil Prices Caused by Iran War Impact Food Costs?” March 10, 2026. https://www.aljazeera.com/news/2026/3/10/how-will-soaring-oil-prices-caused-by-iran-war-impact-food-prices

Al Jazeera. “US-Iran Talks: What’s the Latest on Mediation Efforts?” April 15, 2026. https://www.aljazeera.com/news/2026/4/15/us-iran-talks-whats-the-latest-on-mediation-efforts

Reuters. “Sanctioned Tankers Transit Strait of Hormuz Amid US Blockade.” April 14, 2026. https://www.reuters.com/business/energy/us-sanctioned-chinese-tanker-passes-strait-hormuz-despite-us-blockade-data-shows-2026-04-14/

Iraqi News. “Chinese Oil Tankers Loaded with Iraqi and Saudi Crude Cross Hormuz.” April 12, 2026. https://www.iraqinews.com

Fortune. “Nobel Laureate Paul Krugman Calls It Treason: $580 Million in Suspicious Oil Futures Traded Minutes Before Trump’s Iran Reversal.” March 24, 2026. https://fortune.com/2026/03/24/paul-krugman-treason-oil-futures-trading-trump-white-house/

The New York Times. “Stocks Hit Record High as Wall St. Looks Beyond War.” April 15, 2026.

Reuters / LSEG. Crude Oil Prices Chart and Global Stocks Since Attacks on Iran Chart. April 15, 2026.